Wealth Inequality

Dominant ownership, multiple income streams and a thoroughly skewed money system provide those at the top of the wealth pyramid with incredible power.

The Life and Times of the 1 Percent

- Issue #3

- Author

In 2011, the Occupy movement shone a giant spotlight on growing inequality in the midst of the latest global financial crisis. The scale of the protest — virtually worldwide with over 951 cities participating in 82 countries — was unprecedented. Among other things, the mobilizations drew the public’s attention to the growing wealth and income inequality between the 1 percent and the 99 percent.

Having a long-standing interest in the question of inequality and spurred on by the movement, I decided to take a closer look at the 1 percent in my book The 1% and the Rest of Us. The key questions I wanted to answer were: How can we define or conceive of the 1 percent? Is this vast accumulation of wealth in any way justified or earned? And what helps us explain this vast disparity of wealth?

Identifying the 1 Percent

To answer the first question I decided to look at how investment banks and other financial institutions conceive of the 1 percent. It turns out that their term for the 1 percent is “high-net worth individuals,” or HNWIs. These are individuals who have at least $1 million (USD) invested in income-generating assets like corporate shares, government bonds and real estate. Historically, their numbers have grown over time — but they are still a tiny fraction of global humanity.

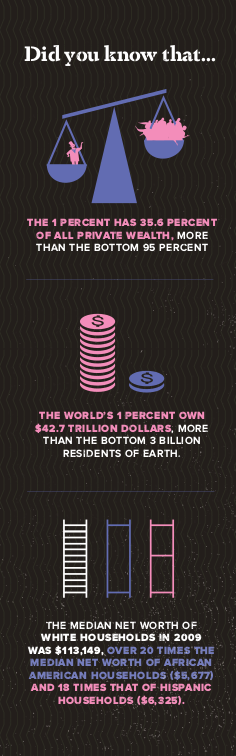

In the latest World Wealth Report by Capgemini and RBC Wealth Management, there were 14.6 million high net-worth individuals. As a percentage of the global population (roughly 7 billion) this means that they constitute a mere 0.2 percent of humanity, or 0.7 percent of adults. So in reality, this class of dominant owners is far smaller than the Occupy movement imagined. But it is also interesting to note the vast disparity even within this small class of individuals. The vast majority — 90 percent — of dominant owners have income-generating assets between USD $1 and 5 million, while mid-tier millionaires with $5-30 million constitute only 9 percent of the HNWI population. This leaves a mere 1 percent of dominant owners with $30 million and above invested income-generating assets.

In the latest World Wealth Report by Capgemini and RBC Wealth Management, there were 14.6 million high net-worth individuals. As a percentage of the global population (roughly 7 billion) this means that they constitute a mere 0.2 percent of humanity, or 0.7 percent of adults. So in reality, this class of dominant owners is far smaller than the Occupy movement imagined. But it is also interesting to note the vast disparity even within this small class of individuals. The vast majority — 90 percent — of dominant owners have income-generating assets between USD $1 and 5 million, while mid-tier millionaires with $5-30 million constitute only 9 percent of the HNWI population. This leaves a mere 1 percent of dominant owners with $30 million and above invested income-generating assets.

It is important to note that the major difference between dominant owners and most of the rest of humanity is that their wealth derives from the power vested in ownership. Most people — if they are lucky — have only one income stream, which derives from their work or labor. The difference between them and the 1 percent is that the 1 percent typically have multiple income streams. Take for example Bill Gates, whose net worth is $90 billion at the time of writing. It may be surprising to some readers to find out that Gates only owns 3 percent of the shares in Microsoft. The rest of his wealth stems from additional income streams coming from Canadian National Rail, Deere & Co., Fomento Economico Mexicano, Republic Services Inc., and Ecolab Inc., just to name a few of his largest equity stakes. It is also worth mentioning that Gates, like others in his class, is what Thorstein Veblen called an absentee owner. He does not physically work in any one of these companies, yet he is able to capitalize their earnings through ownership.

Money and Power

Ownership over multiple income streams gives the 1 percent — particularly those at the top of the wealth pyramid — incredible power. There is a lot of talk about the functions of money, but a clear definition is that it is an abstract claim on society and natural resources represented in a unit of account. What this means in simple terms is that the more income and wealth you have, the greater is your ability to command human beings and natural resources. This has tremendous environmental consequences that are not very well understood at the moment, but the work of Dario Kenner has been a good start in this regard.

The environmental consequences are made all the worse by competitive consumption for status. I use the example of “yacht envy” in my book, where billionaires aim to outdo each other in yacht size and amenities every year. About five years ago, Roman Abramovich’s Eclipse was the largest yacht on the seas. Then in 2013, Azzam, believed to be owned by the President of the United Arab Emirates, was launched and overtook Eclipse in size. Today, there is another super-yacht project underway. At 222 meters and at a cost of US$1.1 billion, it will be the world’s largest and most expensive yacht when launched. This is merely the tip of the iceberg: competitive consumption takes place across a range of goods and services, all with environmental and ecological consequences, not least climate change.

The environmental consequences are made all the worse by competitive consumption for status. I use the example of “yacht envy” in my book, where billionaires aim to outdo each other in yacht size and amenities every year. About five years ago, Roman Abramovich’s Eclipse was the largest yacht on the seas. Then in 2013, Azzam, believed to be owned by the President of the United Arab Emirates, was launched and overtook Eclipse in size. Today, there is another super-yacht project underway. At 222 meters and at a cost of US$1.1 billion, it will be the world’s largest and most expensive yacht when launched. This is merely the tip of the iceberg: competitive consumption takes place across a range of goods and services, all with environmental and ecological consequences, not least climate change.

We also know that the 1 percent always want more money, since the goal of investing is never to lose money but to make more of it. In the theoretical framework I use we call this “differential accumulation.” No owner or investor wakes up in the morning with the goal of making less money today than he or she did yesterday. So whether the 1 percent are actively involved in investment decisions does not really matter; people like Gates and the rest of the HNWI class are participating in the logic of differential accumulation whether they can speak the language of finance or not. They want the value of their owned income-generating assets to increase (rising capitalization), not diminish, and they are likely to have an army of wealth managers trained to do this very task. Differential accumulation is an iron law of capitalism — it is, for lack of a better term, the logarithm of the capitalist universe.

Earning Their Wealth?

This has major implications for political change. So long as the 99 percent remains divided on crucial questions, you can forget about much-needed structural change. The most critical question I identify in my book is whether or not it can be said that these owners earn their income and wealth. How do we know that they do? What theories might we have to demonstrate it? Unfortunately, we do not have any convincing responses from mainstream accounts — or even from Marxists, for that matter.

It is interesting to take a closer look at the disparity, since for most of us all of this is highly abstract. For example, hedge-fund manager David Tepper made $3.5 billion in 2013. The median income in the United States was about $55,000 that same year. So with these two numbers, we can provide a ratio:

1 : 63,636

What this means is that every time our ordinary worker makes another dollar, Tepper will make another $63,636 dollars. Neoclassical theory says this compensation is directly related to the contribution made to production and society. Just on an intuitive level, it is hard to imagine someone being 63,636 times more productive than another human being. Of course there are real differences in talents, skills and abilities. No one should deny it. But they certainly are not that drastic and evolution does not work faster in one human than another to such an extreme degree.

By this scale of differential income, Tepper should be considered an X-Man with real superpowers. But of course, he is just a man in a particular position in society able to redistribute income to himself and his investors. Consider, for example, the differences between a professional marathon runner and an average Joe who will walk a marathon. Obviously there will be a massive difference in skill and ability and talent. So what do you think the ratio will be? The world record for male marathon running is 2:02:57 hours set by Kenya’s Dennis Kimetto in Berlin in 2014. If average Joe walks a marathon, how long would it take? Estimates vary, but if we walked at 20-minute miles it would take about 8.7 hours. So what is the difference between a highly skilled marathon runner and average Joe? Turns out the ratio is:

1 : 4.35

We could all agree that Kimetto is a little over four times faster or better at running than an average person who simply walks the marathon. Kimetto undoubtedly deserves to be the world record-holder. But in no way is Kimetto 63,636 times faster or more talented than the average person walking a marathon. So something is seriously askew when we look at these ratios of inequality — and I believe it is the task of critical political economy to challenge what I call “the superman theory of wealth accumulation,” or the radical anti-social belief that wealth is earned solely on the basis of individual knowledge, talents and skills. Since this type of thinking is engrained in much of Anglo-American culture, I believe that that the 99 percent has its work cut out for it in popularizing the idea that all wealth is social and can only ever be social. Only once we realize this can we start to think about how wealth might be distributed in a democratic and free society.

The Money System

But another factor — often overlooked — also contributes to the growing disparity between the 1 percent and everyone else: the way in which new money enters our economies. This is not the place for a lengthy exegesis on money mechanics, but suffice to say that it is now well established that banks create new money when they issue loans at interest. Since most banks lend against income streams, accumulated wealth or collateral, the already wealthy are at a massive advantage when it comes to taking out new loans. This money can be used to capitalize additional income-generating assets, exacerbating pre-existing inequalities. For example, it is stated that the leading hedge-fund managers can leverage their capital by a multiple of 10. In other words, $1 billion can become $10 billion to speculate with. Inequality is exacerbated precisely because those with no assets, little assets or average incomes cannot get access to the similar amounts of money and credit. So there is an advantage for the 1 percent built into the modern money system and a systematic disadvantage for the part of the 99 percent who have little or no access to credit.

But another factor — often overlooked — also contributes to the growing disparity between the 1 percent and everyone else: the way in which new money enters our economies. This is not the place for a lengthy exegesis on money mechanics, but suffice to say that it is now well established that banks create new money when they issue loans at interest. Since most banks lend against income streams, accumulated wealth or collateral, the already wealthy are at a massive advantage when it comes to taking out new loans. This money can be used to capitalize additional income-generating assets, exacerbating pre-existing inequalities. For example, it is stated that the leading hedge-fund managers can leverage their capital by a multiple of 10. In other words, $1 billion can become $10 billion to speculate with. Inequality is exacerbated precisely because those with no assets, little assets or average incomes cannot get access to the similar amounts of money and credit. So there is an advantage for the 1 percent built into the modern money system and a systematic disadvantage for the part of the 99 percent who have little or no access to credit.

This disparity will likely continue because it is structural or systematic and the political opposition is largely fragmented. Unless people organize and push for structural change, particularly on how we produce new money as debt in the economy, change will continue to happen, but only at the margins. The worst-case scenario is that we continue on our current path, destroy the environment for future generations in the process and through the practices of differential accumulation, experience an even greater gap between the 1 percent and the rest of us. There are waves of hope that this scenario can be avoided — but at the moment, they are just waves, not the tidal force we need.

Source URL — https://roarmag.org/magazine/debt-money-power-inequality-one-percent/

Next Magazine article

The Debts of the American Empire — Real and Imagined

- Cassie Thornton, Max Haiven

- September 21, 2016

Fancy Forms of Paperwork and the Logic of Financial Violence

- David Graeber

- September 21, 2016

Digital subscriber

Digital subscriber  Print & Digital subscriber

Print & Digital subscriber