Politicizing Debt

By revealing the social and political nature of financial markets, debt audits could become an important weapon in the arsenal of debtors’ movements.

The “Golden Noose” of Global Finance

- Issue #3

- Author

The battle between Greece and its creditors may have disappeared from the media spotlight, but the crisis has not gone away. The latest round of pension reforms and VAT hikes has been accompanied by renewed protests against the supposedly left-wing Syriza government. Look to the opposite corner of Europe and we find the UN issuing warnings that UK austerity policies, including benefit reforms, are in breach of the country’s international human rights obligations. And everywhere the pain of further belt-tightening by neoliberal policymakers is blamed on migrants, minorities, the unemployed and disabled.

What all these different contexts have in common is that the problem is not one of states or whole economies running out of money. Rather, social wealth is being directed from households and the public purse to the financial sector in the form of debt repayments — even if it is not always clear what exactly is being repaid, as those bearing the costs of adjustment often did not take the loans in the first place. When basic needs are not met because money is flowing to banks instead, it is time to start questioning the legitimacy of these debts and the broader financial system under which they were incurred.

Coercion and Control

The financial sector lies at the heart of many of humanity’s most pressing problems — from investment in fossil fuels and arms sales to the extraction of immense wealth from society, resulting in the rise of inequality and the hollowing out of traditional democratic processes. Although we already seem to have moved on to a new era of permanent austerity, in which further cuts to public services hardly need to be justified, it is worth remembering that the original justification for such measures stemmed from the bank bailouts.

In truth, of course, the story did not start in 2008. The deregulation of financial markets, a key component of the neoliberal agenda since the 1980s, had already resulted in a massive financial expansion by the end of that decade. It created the conditions for the engineering of products so complex that in the end their face value had little to do with any underlying values in the “real” economy. Derivatives markets ballooned to outdo ordinary product markets manifold; they became a seemingly endless pit where financiers could hide unpayable debts and keep the accumulation of fictitious capital going.

In truth, of course, the story did not start in 2008. The deregulation of financial markets, a key component of the neoliberal agenda since the 1980s, had already resulted in a massive financial expansion by the end of that decade. It created the conditions for the engineering of products so complex that in the end their face value had little to do with any underlying values in the “real” economy. Derivatives markets ballooned to outdo ordinary product markets manifold; they became a seemingly endless pit where financiers could hide unpayable debts and keep the accumulation of fictitious capital going.

Rather than a mere by-product of the system, debt has from the beginning of the neoliberal project been a key tool for subjecting and incorporating countries and communities which often had little to gain from the brave new world of finance. This goes for entire states, like Argentina and Greece, as well as the ordinary households that are now forced to borrow to cover basic expenses — whether it is through payday loans, credit cards, student finance or the infamous sub-prime mortgage lending that fed into the Wall Street crash of 2008.

Drawing such a direct parallel between household debt and public debt may seem odd to those of us schooled in heterodox economics. After all, we have spent much of our time in the past years trying to convince people that — contrary to what neoclassical economists imply when they seek to justify austerity measures — these two levels of economic activity are not comparable: unlike a household, a country cannot live beyond its means, as it always retains the ability to print money or raise taxes in order to service its debts. But debt is not purely an economic phenomenon; it also has important social and political dimensions. Looking at it from that perspective, despite important differences in the economics, the mechanisms of coercion and control are very similar whether it comes to household or public debt.

Illusions of Wealth

Nothing illustrates these disciplinary mechanisms and the central role of debt in neoliberalism better than the bout of subprime mortgage lending in the US during the mid-2000s. It provided people with no job, no income or no assets the opportunity to buy into the heavily marketed American dream of homeownership. After the crash, these poor, marginalized and often Black communities found themselves on the losing side of a gamble that had been imposed on them. Yet it is they who were blamed for their supposed profligacy.

More generally speaking, debt has for the past four decades enabled those of us in the Global North to keep buying and consuming even as real incomes remained stagnant or steadily declined. Without the illusion of wealth generated by easy access to credit cards, interest-only mortgages, consumer credit and car loans, there would have been little left of the “middle class” by the turn of the century. Neoliberalism’s inherent drive to concentrate all wealth into the hands of the few would have been self-evident to the average citizen a long time ago.

A similar illusion of wealth — and a similar obfuscation of power relations — appears at the global scale. The richest economies in the world actually produce very little. Consumption largely relies on the provision of international credit and the continuous inflow of cheap commodities from the Global South. Yet those countries trapped at the unfavorable end of this international division of labor have little power to change their situation, as they find themselves trapped in neoliberal economic policies and a global financial architecture that keep them impoverished and dependent on foreign investment.

Many of these neoliberal policies and financial dependencies are the direct result of the conditions imposed in return for international loans. The Third World debt crisis of the 1980s — triggered by a dramatic hike in the US interest rate — was remedied by the US government and international financial institutions dictating developing countries to cut public services, privatize state assets and liberalize trade and capital accounts. Only then were these countries able to borrow the money needed to repay the original debts, which were unpayable either way. With economies stagnating and the loans accumulating interest, countries in the Global South have repaid $7.50 for every dollar they owed in 1980, yet they still owe $4 more.

The austerity recipe first applied in the 1980s, however destructive for the debtors, proved so lucrative for the lenders that when the crisis finally moved to Europe in 2010, the International Monetary Fund and the Eurozone creditor nations imposed very similar conditions on the heavily indebted countries of the periphery, most notably Greece. As before, the result was not economic recovery but a humanitarian crisis that pushed millions into dire poverty and brought back illnesses long eradicated. Even the IMF now acknowledges that Greece cannot possibly repay all its debts, and it has even admitted that the original bailout served as a “holding operation” to allow private lenders to escape without losses.

Politicizing Debt

The similarities between austerity in Europe and structural adjustment in Africa, Asia and Latin America are important because they show that hiding human rights violations and the dismantling of welfare provisions behind the cloak of technicalities is not the exception but the rule. It is what keeps the bondholding class in its position of unrivaled structural power. Hence it is not surprising that demands for the non-payment of illegitimate debts stretch across decades and continents — and have emerged anew since the latest crisis.

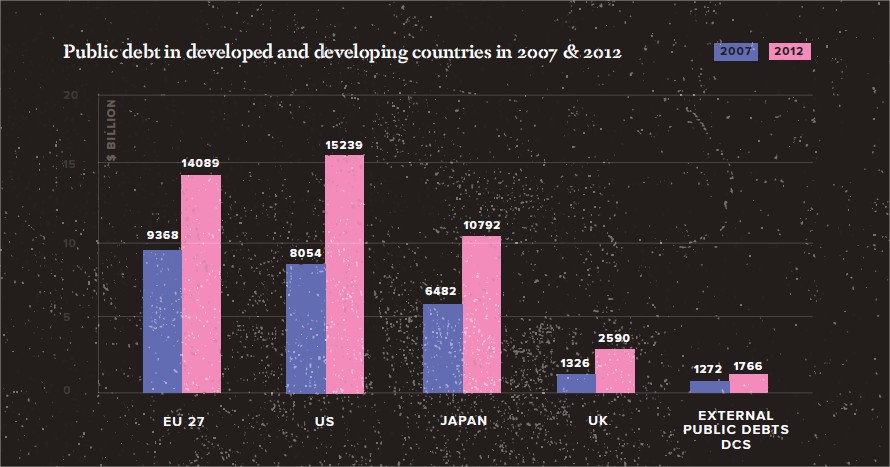

Via CADTM World Debt Figures 2015

Last year, the Greek Truth Committee on Public Debt declared much of the country’s debt load to be illegal, illegitimate and odious. In Spain, after several municipalities were taken over by progressive coalitions last year, Madrid has become the first city to start a participatory debt audit with an initial focus on corruption. Research by a group I am part of, Debt Resistance UK, is enabling residents in councils across England, Scotland and Wales to object to their council’s risky and expensive borrowing from banks. All these projects stand on the shoulders of past movements in the Global South, which have done much to elucidate the social and political nature of global financial markets.

The paradox of the supposedly neutral yet disciplining market is obvious. If “the market” is like a natural phenomenon, stripped of its social and distributional dimensions, then why does it react so strongly to political events? Why does a change in government in Greece or Portugal send interest rates on a roller-coaster ride?

Political economist Susanne Soederberg rightly describes this global financial architecture as a “golden noose.” The noose has to be tight enough to prevent debtor countries from delinking from the international credit system whilst simultaneously enabling their “socioeconomic strangulation.” In short, “to recreate the power relations within the international credit system it is necessary to ensure that debtors are kept within the lending game.” But if neoliberalism and the seemingly apolitical language of debt and finance have enabled this balancing act, then the spell can be broken by politicizing debt. And debt audits do precisely that. A debt audit starts to ask questions: How was the debt accumulated? By whom? Who made or advised on the decisions? Who benefited from the spending of the borrowed money?

In Greece, the answers to those questions in the preliminary report of the Truth Committee showed that most of the country’s bailout had gone directly to the financial sector and had not benefited the Greek people. They also showed that the conditions imposed on the loans were often in violation of the EU’s own laws. If the Truth Committee had had more time and resources, it could have undertaken a full audit of the country’s public debt and the international bailouts — but it was cut short after Syriza decided not to use the findings of its preliminary report as an argument in the negotiations with the Troika of foreign lenders.

Ecuador was more successful in 2008. After a public debt audit initiated by President Rafael Correa when he came to power, the country defaulted on $3.2 billion owed to international creditors, freeing up the funds for social spending. Ecuador’s was a bold stance. The power of vested interests, the disciplinary force of global financial markets and the revolving door between international institutions, domestic politics and private banks give everyone involved a stake in the hiding game. That indebtedness is so often understood to be the fault of the debtor does not help in acting on this predicament.

At Debt Resistance UK, our work started from a member stumbling across an obscure acronym in local authorities’ balance sheets: a “LOBO.” This prompted us to dig deeper into this type of loan, called a “Lender Option, Borrower Option,” but in reality an expensive bet on interest rates. We argue that LOBOs are not legitimate, and possibly even illegal, for a council to take on. Yet we found a total of £15 billion of LOBOs accumulated by councils across the British Isles. When trying to obtain the contracts, we discovered an interesting mix of vested interests and borrower stigma. The information was difficult to get hold of despite Britain having a Freedom of Information Act that ensures transparency in the public sector — although that law is in the process of being repealed. After contesting a myriad of rejections to obtain the loan contracts and publicizing the ways in which residents can take action to contest them, it seems we have hit another obstacle in this pseudo-democratic system. The ball is now in councils’ auditors’ court, and as it turns out, local authorities are audited by the same big accountancy firms as the banks that issued the loans we are contesting.

The complex nature of financial institutions often appears like the antithesis of transparency, and using loopholes in the system to challenge them can seem overly bureaucratic. Still, precisely because of this, engaging the public is an important part of a debt audit, which is why Madrid is exploring ways to realize its audit in a participatory manner and why the Greek Truth Committee’s work was broadcast directly through the Parliament’s TV channel. The educational aspect of debt audits is in a way more important than lobbying decision-makers through available political channels, because the work is about breaking down existing power structures. The road to a more democratic system needs to be both radical and accessible, or else it is likely to be flawed from the very start. Without transparency and participation, we risk replacing those in power instead of dismantling the underlying power relations.

Debt-as-Exploitation and Debt-as-Oppression

The potential of collective action against financial exploitation is not just limited to public debt: it also extends to the realm of private debt. Here as well, the language and morality of indebtedness serves to atomize borrowers and makes distressed debtors believe their predicament is their own fault. The key to breaking that individualizing experience is to find power in our common condition: under neoliberalism, most of us are debtors. Just as wage laborers organized to counteract isolation and fight against exploitation at the point of production, so we can organize as debtors and use our collective power to hold our creditors accountable and reclaim our social wealth.

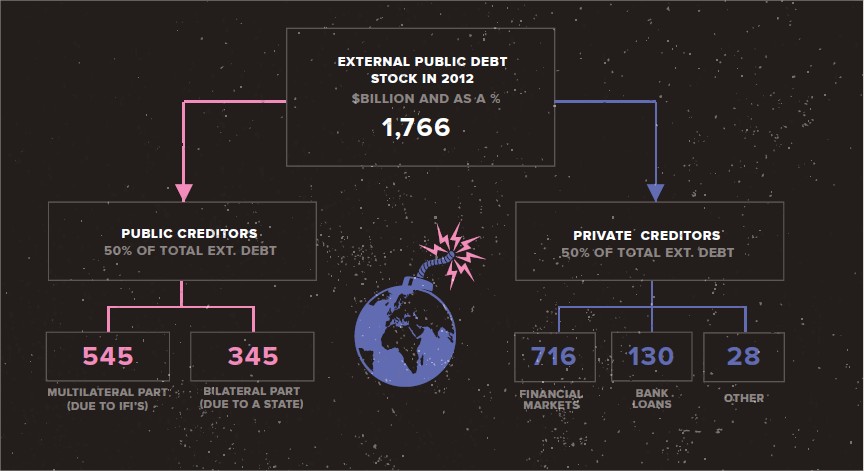

Via CADTM World Debt Figures 2015

The first step is to see through the political decisions and socio-economic structures that have led to such vast increases in private indebtedness. For one, when national or local governments — enthralled to the neoliberal dogma that public debt levels must be reduced — cut welfare spending, it is individuals and households that pick up the bill. While public services are privatized, the liabilities of the financial sector are socialized. In the process, we are compelled to further indebt ourselves. In the UK, for instance, one of the first measures of the Conservative-led government that came to power in 2010 was to triple university tuition fees and introduce a real interest rate on student loans. This has led to an average increase in the debt burden of new graduates to an estimated £44,000. Nearly half of the resultant debts will never be repaid. The value or quality of education, of course, has not increased — yet the pressure on graduates to obtain well-paid jobs and work “within the system” has.

Extreme examples of personal debt also come from the other side of the Atlantic, where the public provision of services is even more absent. Student debt in the US stands at more than $1.3 trillion and has already led to hundreds of thousands of defaults — with for-profit colleges unsurprisingly over-represented in default statistics. But given the shared experience and common conditions of the individual debtors, students also find it easier to organize resistance than those trapped in skyrocketing credit card bills or those forced to turn to payday lenders to bring food to the table. As they write in their article in this ROAR issue, the Debt Collective — a legacy of the Occupy Wall Street movement — took organizing against student debt to new heights last year when graduates from for-profit Corinthian Colleges went on a debt strike to demand the cancellation of their student loans because the degrees from their collapsed schools are literally worthless.

Beyond its exploitative side, debt also has important oppressive dimensions. A look at the US subprime mortgage crisis shows this very clearly. In a 2013 article, political economist Adrienne Roberts illustrated how racist and sexist the seemingly apolitical notion of risk really is. Over half of all subprime loans prior to the 2008 financial crisis were given to people with credit scores high enough to obtain conventional loans; on average these people paid an estimated $85,000 to $186,000 more in interest. Subprime lenders specifically targeted women and minority groups, leading to a situation in which an African American with the same income and credit risk as a white person was up to 34 percent more likely to be sold on to a subprime mortgage. The intersectionality of different forms of oppression means that, whereas an African American woman is over 5 percent more likely to receive a subprime mortgage than an African American man, this likelihood trumps a white man’s by 256 percent. All of this in blatant violation of the 1974 Equal Credit Opportunity Act — itself an outcome of long-standing struggles for equal access to credit by the women’s rights and civil rights movements — which explicitly bans discrimination on the basis of gender or race.

Roberts also writes of the interconnectedness of different debts: she quotes a survey that found that 29 percent of low- and middle-income households in the US with credit card debt linked it to healthcare expenses. Over half of medically indebted households that took out second mortgages or refinanced their homes in 2005 used the money to pay down credit card debt. Anybody with a credit card would know that this is not a sustainable way to cover major expenses, but one of the inequality-breeding paradoxes of finance is that the ones who need credit most generally get it at the worst terms. The lower your credit rating, the higher your interest rate. If you do not have a credit card, payday lenders or loan sharks are your only option. Again, theory tells us that interest is the price charged by lenders for the risk of non-payment, which makes usury sound legitimate.

Breaking Out of the Golden Noose

Despite the self-evident fact that not all debtors have made an informed and voluntary choice, the belief that debts always have to be repaid is widely held. But what is a debt? As the anthropologist David Graeber writes in Debt: The First 5,000 Years, the difference between a monetary debt (to a bank, for instance) and a moral obligation (of the type “I owe you a favor”) is that the former can be precisely quantified. Considering that putting numerical values on things that cannot really be quantified — such as uncertainty over the creditworthiness of a borrower — is at the heart of what the financial sector specializes in, it is not surprising that the language around debt remains inaccessible and in that sense undemocratic. Until we tackle it, that is, and point our fingers at each detail of a loan contract.

According to Graeber, another key feature of debt is the fact that the promise to repay can, in the final analysis, only ever be enforced by violence. The threat of violence — in home repossessions or wage garnishments, for instance — is not just needed to uphold the creditor-debtor relation; it is also a key pillar of the neoliberal political order more generally. Indeed, austerity itself is a form of violence, inflicting grave physical suffering and leading to violent conflicts around the globe: from the IMF riots of the 1980s to the student marches and occupations in London in 2010 on to the sustained social unrest in Greece and beyond.

All of this clearly reveals the fiction at the heart of the idea of “the market” as a set of neutral, self-organizing and apolitical processes that spontaneously emerge whenever the state is rolled back. In reality, and especially in times of crisis, markets can neither arise nor survive without state-sanctioned violence. Politicizing the seemingly technocratic decisions that are taken under the cloak of economic necessity is an important first step towards liberating ourselves from that violence and breaking out of the “golden noose” of global finance. As the resultant struggles progress, debt audits and coordinated defaults may come in as increasingly powerful weapons in the arsenal of the world’s budding debtors’ movements.

Source URL — https://roarmag.org/magazine/golden-noose-global-finance/

Next Magazine article

The Potential of Debtors’ Unions

- Debt Collective

- September 21, 2016

The Debts of the American Empire — Real and Imagined

- Cassie Thornton, Max Haiven

- September 21, 2016

Digital subscriber

Digital subscriber  Print & Digital subscriber

Print & Digital subscriber