Beyond Resentment

Dethroning the financial aristocracy will require more than moral outrage and tinkering at the margins. We need to push for deep, structural change.

Defeating the Global Bankocracy

- Issue #3

- Author

Bankers have never really been a very popular lot. Resented by the land-owning aristocracy, the puritanical clergy and the laboring popolo minuto alike, the moneychangers of renaissance Florence were punishable by torture if they dared to defraud their unsuspecting customers. In his Inferno, Dante reserved a special place for usurers on the seventh circle of hell, where sinful lenders with charred faces would sit still in the burning sand for all eternity, under whipping winds and rains of fire, weighed down by the moneybags around their necks.

In a similar vein, when supporters of the Dominican friar Girolamo Savonarola ran for office on an anti-Medici platform in the late-fifteenth century, the radical preacher’s campaign stunt involved the burning of luxury items and symbols of wealth on his “bonfire of the vanities.” Such moral outrage at the emerging bourgeoisie — and the class of idle rentiers it spawned — was deeply engrained across the Old Continent. In medieval Barcelona, for instance, bankers who went broke were publicly humiliated by town criers and forced to survive on bread and water until they had fully reimbursed their depositors. Those who failed to do so within a year were beheaded in front of their counter — which is precisely what happened to an unfortunate Catalan banker named Francesch Castello in 1360. Parenthetically, the words “broke” and “bankrupt” have their origins in the Old Italian banca rotta, or “broken bench,” referring to the moneylenders whose exchange counters had metaphorically collapsed under the weight of their liabilities.

If cheating the little people or simply “breaking the bank” was sure to lead to decapitation or torture in the city’s dungeons, messing with the nobility was certainly out of the question. The Knights Templar learned this the hard way early on: when they insisted that Philip IV of France repay the debts he had incurred for the dowry of his sister and the quelling of a domestic tax revolt, the king simply had his lenders rounded up and burned at the stake. Seen in this light, the Bardi and Peruzzi of Florence were probably lucky to be out of reach of King Edward III’s troops — but they still suffered massive financial losses when the English monarch repudiated his debts after the Hundred Years’ War. Their respected family banks, once the most formidable of Europe, went bust not long after in the economic depression of the 1340s. Later, a branch of the Fugger of Augsberg, a mighty banking dynasty in the Holy Roman Empire, suffered a similar fate following the serial defaults of King Philip II of Spain.

In the very early days of capitalism, then, private financiers were still relatively powerless in the face of sovereign authority and often held publicly accountable for immoral behavior or irresponsible lending. They most certainly were not seen to be “doing God’s work,” as the most universally despised banker of our times — Lloyd Blankfein of Goldman Sachs — would have it. So what changed? Barring the general reluctance to engage in cruel medieval methods of punishment, why is it that we can no longer seem to hold private lenders accountable for their immoral behavior? Why did we allow them to escape unharmed in 2008, while the rest of us bore the consequences? Surely the answer has something to do with the vast increase in the bankers’ power over the years. But where does this power come from? What are its sources, how did it evolve — and how can it be resisted and overcome?

The Sources of Financial Power

Political economists have long debated the sources of financial power — and of business power more generally — in capitalist societies. While these debates have often been fairly technical or carried out at a high level of theoretical abstraction, they cannot be dismissed as irrelevant or merely “academic.” Identifying the sources of corporate influence on economic policymaking and social life matters because our answers to these questions shape the type of solutions we come up with in the attempt to democratize our societies.

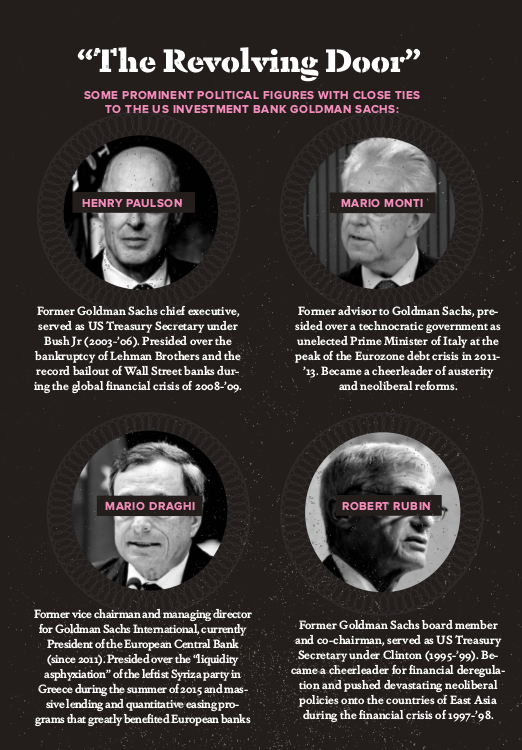

One interpretation of financial power commonly found in liberal circles centers on personal connections, lobbying and the role of “money in politics.” It blames the “corruption” of the democratic process and the failure to hold the financial sector accountable on “regulatory capture” and the “revolving door” between Wall Street and Washington. It also tends to denounce the failure of free-market ideology and the faulty assumptions of neoclassical economics — especially its Efficient Markets Hypothesis and its metaphysical belief in “expansionary contractions” — for making European leaders buy into the “dangerous idea of austerity,” or tricking US policymakers into believing that what is good for Wall Street is good for America (and by implication for the world). Prominent exponents of this line of thinking include the Nobel Prize-winning economist Joseph Stiglitz and the reformed ex-IMF chief economist Simon Johnson.

The solution that naturally flows from this position is straightforward: impose strict regulations on public staffing and corporate lobbying to establish a firewall between policymakers, regulators and the financial sector; restrict campaign finance to “take money out of politics”; and promote a more heterodox — that is to say, Keynesian or post-Keynesian — approach to the study of finance to ensure that the next generation of leaders will at least have some macro-economic sense drilled into their heads in college or business school. Going further, the more systemically-minded critics of finance may highlight the fact that many important institutions are simply “too big to fail,” to which the answer would be the breaking up of these firms and the introduction of strict limits on company size. This was basically Bernie Sanders’ position.

The solution that naturally flows from this position is straightforward: impose strict regulations on public staffing and corporate lobbying to establish a firewall between policymakers, regulators and the financial sector; restrict campaign finance to “take money out of politics”; and promote a more heterodox — that is to say, Keynesian or post-Keynesian — approach to the study of finance to ensure that the next generation of leaders will at least have some macro-economic sense drilled into their heads in college or business school. Going further, the more systemically-minded critics of finance may highlight the fact that many important institutions are simply “too big to fail,” to which the answer would be the breaking up of these firms and the introduction of strict limits on company size. This was basically Bernie Sanders’ position.

Needless to say, all the above would be quite helpful in loosening the stranglehold of finance and of neoliberal ideology on the existing democratic process. But if these solutions ultimately seem rather cosmetic, it is because they are the logical corollary of theoretical explanations that, in the final analysis, fall short in identifying the deeper source of the problem. In a way, many liberal critics of Wall Street get causality the wrong way around: they argue that finance is powerful because so many bankers hold positions of political influence, have direct access to policymakers, and have successfully shaped the political narrative. In truth, however, bankers are not just powerful because they are “in government” — they are in government because they are powerful.

Gatekeepers of Credit Access

In my own research, including a forthcoming book on the power of finance in sovereign debt crises and ongoing work on the historical proximity of bankers to policymakers, I distinguish between the “instrumental” forms of power deployed by the finance industry and its underlying structural power. These two are not mutually exclusive: instrumental forms of power like lobbying, campaign donations and direct staffing of key government positions remain very important channels of political influence. But these more personal and more overt forms of influence are undergirded by a much deeper and less visible source of power that goes to the very core of what capitalism is about: the accumulation of capital. To reproduce itself over time and fulfill its need for constant expansion, the system depends on a healthy and uninterrupted flow of credit. And if credit is the lifeblood of the capitalist economy, the banking sector is its beating heart.

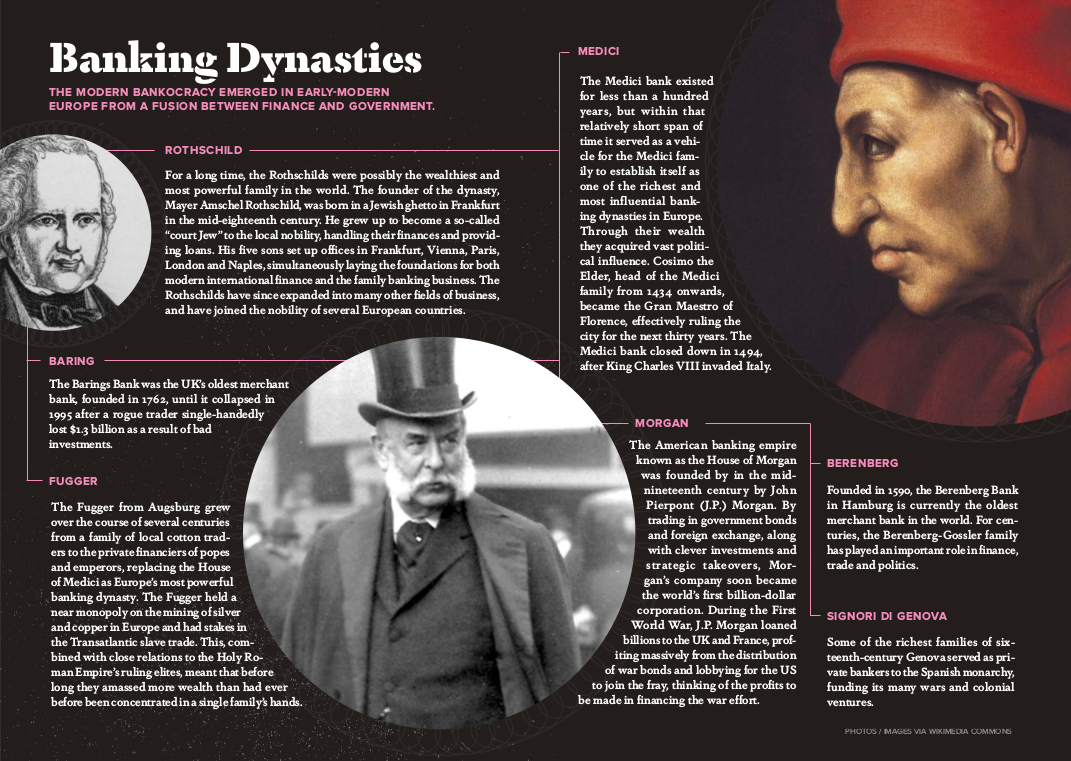

The sway that finance holds over politics and society is therefore ultimately a product of its structural position in the capitalist economy. The exact nature of this position is not pre-determined; it is historically contingent on the outcome of major events like wars and revolutions, and constantly reshaped by economic conjunctures, the ever-shifting balance of power between different social forces, and the ideational and institutional legacies they leave behind. But one constant throughout the history of capitalism is for the role of credit-provision to eventually become concentrated and centralized in the hands of a small group of private financiers — traditionally large dynasties like the Houses of Medici, Rothschild and Morgan, but nowadays mostly powerful international corporations like Deutsche Bank, HSBC and Bank of America.

This tendency towards concentration and centralization in the credit system renders everyone else in capitalist society — states, firms and households alike — increasingly dependent on an ever-smaller number of private banks and financial institutions for their own reproduction. The result is to endow a limited number of giant financial firms with the position of private gatekeepers to market access, ensuring that everyone else will have to accept and adhere to their demands and conditions if they are to survive economically.

This is why we must be careful not to personalize the problem. Modern society is simply not the same as the fading Christian lifeworld that inspired Castello’s beheading and Dante’s Inferno. There are epochal differences here that hint at the limits of the “politics of resentment” and its logic of moral outrage in our times. Unlike the feudal order that preceded it, contemporary capitalism is a system of impersonal domination in which social power is largely mediated by the abstract expression of value: money. Thus poor Savonarola ended up torched on his own bonfire, his moralism rendered mute by the superior class power of the moneyed Medici family. Today, the financial aristocracy no longer needs to burn its opposition at the stake; it is the abstract violence inherent in the global financial system that compels us all to play by the rules of the game. But if that’s not enough, there’s still the violence of the state to back it up.

Credit Asphyxiation as a Weapon

To see what happens when a sovereign state and an entire people refuse to abide by the conditions laid down by global finance, prompting a cartel of public and private lenders to actively exercise their gatekeeping function in order to bring the delinquents back in line, look no further than Greece in the summer of 2015. Unlike in previous historical eras, private bondholders and European creditors did not need to resort to the instrumental power of gunboats to bring the Syriza government to its knees. After a tense six-month standoff in which they had slowly asphyxiated the Greek state by halting the flow of credit, all they had to do was stop the provision of further emergency liquidity to the country’s fragile banking system. The next morning, as citizens across the country lined up in front of ATMs to withdraw their precarious savings, the government was forced to shut down the banks and impose strict capital controls.

The results were just short of catastrophic. The Greek economy effectively ground to a halt: industries were no longer able to obtain trade credits to acquire key inputs, many employers stopped paying wages and production came to a standstill. Had this credit embargo continued much longer, the results would have been disastrous, as the government had not prepared any contingency plans on how to import oil or medicine after strategic reserves would run out, nor on how to ship water and energy to arid islands or distribute food from the countryside to the city once stocks would be depleted. If credit circulation constitutes the blood flow of a capitalist economy and the banking system its beating heart, Greece was having a massive heart attack — deliberately provoked by its own money doctors to force it to desist. The widespread moral outrage expressed in the subsequent referendum, in which 61.8 percent of Greeks voted to reject the creditors’ ultimatum, was summarily dismissed — its implications simply shoved aside.

Dramatic developments like these have prompted a number of commentators to highlight the growing incompatibility between capitalism and democracy under conditions of financialization. As Germany’s pre-eminent economic sociologist Wolfgang Streeck has convincingly demonstrated in his book Buying Time, the long-standing conflict between the Marktvolk of private creditors and the Staatsvolk of ordinary citizens has in recent years been decisively settled in favor of the former. But while Streeck presents the preceding evolution of the “debt state” and the more recent rise of the European “consolidation state” as a relatively novel political development, its systemic roots actually go back to the very origins of capitalism and the concurrent emergence of the capitalist state, public debt and the first private and central banks in early-modern Europe.

To truly grasp the nature and scope of our present predicament, it would therefore be useful to follow scholars like Fernand Braudel and Giovanni Arrighi in familiarizing ourselves with the longue durée of capitalist development — a process that has unfolded over eight centuries and that, for our purposes here, can be divided into three distinct stages, each of which has allowed finance to successively extend its sway over political authority; over economic production and the global periphery; and finally over social reproduction and everyday life.

1) The State-Finance Nexus

The first phase of capitalist development, which began in the European city-states of the late-medieval period, was marked by the gradual decline of the personal power of feudal sovereigns and the growing impersonal power of a moneyed merchant elite. While the court lenders of the middle ages had derived much of their political influence from their direct and exclusive access to kings and princes, the intensification of inter-state rivalry over the centuries gradually increased the reliance of sovereigns on other sources of financing. Since trade competition and military conflict were especially fierce on the Italian peninsula, where local rulers presided over a number of important city-states, the latter increasingly depended on mercenary armies to fend off foreign invasions, claim new territories and trade routes, and maintain the regional balance of power.

But if mercenaries for self-defense were expensive, empire-building was even more so. Thus the rulers of small cities with big ambitions — like Venice, Genoa and Florence — grew increasingly dependent on taxation and credit: what Cicero famously called the “sinews of war.” For this, they turned towards the emerging middle class of propertied merchants and merchant bankers, which in turn prompted powerful demands for political representation. Over the course of the following centuries, the growing dependence of city-states on credit and the resultant struggles over taxation, debt repayment and political rights gave rise to a number of financial and institutional innovations that would dramatically transform the nature of political authority, the economic structure of society and the relation between the emerging merchant class and the landed nobility. The first and most foundational of these was the development of the public debt in Venice and other city-states sometime in the twelfth century.

In Capital, Marx identified this moment as a historical landmark, noting that the rise of the public or national debt — which he also referred to as “the alienation of the state” by private financiers — “marked with its stamp the capitalistic era.” Over time, the process gradually ate away at the vested power of the nobility and the Church and gave rise to the first bourgeois republics, with representative institutions centered on local merchant oligarchies. For some time, these small proto-capitalist city-states managed to spectacularly outcompete the massive feudal kingdoms and landed aristocracies of Old Europe in both trade and war, thanks in large part to their superior capacity to attract credit at affordable interest rates.

On the back of the system of public credit and the first national banks — founded to manage the resultant national debts — in turn arose a complex continental network of merchant banks. After early endeavors by the Bardi and Peruzzi of Florence faltered, the art of international banking was first properly perfected by the Genoese, who developed an ingenious system of syndicated lending to Philip II of Spain that financed his many wars and colonial conquests in Europe and the Americas while bringing untold riches to the Ligurian coast. Despite the king’s repeated defaults, this Ibero-Genoese alliance is generally recognized as the first successful regime of cross-border private-public contract enforcement, marking a seminal shift in the balance of power between mighty sovereigns and their foreign creditors.

At the same time, the rise of the public debt also served to dramatically transform political authority inside the city-states themselves, effectively turning the evolving state apparatus into a wealth-collection machine for the rising bourgeoisie, redistributing vast sums of the social product from the public purse to private pockets. This is why Marx considered the development of the public debt to constitute “one of the most powerful levers of primitive accumulation.” At the same time, he also recognized how it prepared the ground for the eventual rule of finance, noting how “the national debt has given rise to joint-stock companies, to dealings in negotiable effects of all kinds, and to agiotage, in a word to stock-exchange gambling and the modern bankocracy.”

This modern bankocracy, which David Harvey has also referred to as the “state-finance nexus,” found its most explicit expression in renaissance Florence, where the Medici family took the fusion between concentrated financial power and nominally independent governmental authority to unprecedented heights. Yet by driving their political ambitions to the extreme — even having four members of the House of Medici elevated to the papacy and two made Queen of France — the Medici ultimately rendered their power too personal. Even as their pet project of attaining supreme control over Florence flourished, their financial empire floundered. It was only in the merchant bastions of Genoa and later Amsterdam that the impersonal rule of finance reached its early apogee.

2) Finance Capital and Imperialism

In the seventeenth century, after the decline of their Italian competitors and the defeat of the Spanish in the Eighty Years’ War, the Dutch took international finance to new heights with the creation of the first stock exchange, the founding of the first multinational joint-stock corporation (the East India Company), and the development of international capital markets. As a result, the city of Amsterdam, controlled by an ethnically diverse oligarchy of merchants and bankers, firmly established itself as Europe’s first financial center — until it was gradually displaced by London and Paris in the late eighteenth and early nineteenth centuries, with the English assuming the mantle of “banker to the world” and the French coming in second as banker to the continent.

This new phase in capitalist development, which properly took off with the industrial revolution in Great Britain and the displacement of the Dutch by the English as the dominant colonial, maritime and commercial power, again witnessed a number of financial and institutional innovations: from the expansion of international capital markets to the creation of the classical gold standard. This in turn opened up two major new outlets for investment — domestic firms and peripheral states — which allowed finance to consolidate two additional bases of power: industry and empire. In the latter third of the nineteenth century, the first gave rise to what Hilferding called “finance capital”: the monopolistic confluence of productive and banking interests as a result of money capitalists taking ownership of industrial firms. The second led to what Hobson called the “export of capital”: vast sums of money flowing from core to periphery, especially the newly independent states of Latin America and the Mediterranean, where investors hoped to find higher yields than they could extract from the increasingly saturated markets at home. These developments reached their climax in the so-called “first wave of globalization” under the Pax Britannica of the classical gold standard era.

As Karl Polanyi powerfully portrayed in The Great Transformation, this was to become the hour of haute finance, made up of formidable international banking dynasties like the House of Rothschild and the House of Morgan, which collectively served as “the main link between the political and the economic organization of the world.” Building on the state-finance nexus that had already been established in the mercantile period, haute finance expanded its sphere of influence and took its established power position to new heights through its close ties to industry and its hold on foreign states. Polanyi noted how the Rothschilds, in particular, “were subject to no one government; as a family they embodied the abstract principle of internationalism; their loyalty was to a firm, the credit of which had become the only supranational link between political government and industrial effort in a swiftly growing world economy.”

Taken together, the rise of finance capital — or haute finance — and the increasingly competitive search for profitable investment opportunities abroad eventually gave rise to high imperialism, which was analyzed most prominently by Lenin, Bukharin and Luxemburg. This period between 1870 and 1914 witnessed the penetration of finance into the global periphery, facilitated by the prominent role of the state in settling international debt disputes and intervening on behalf of bondholders and other investors: from the use of gunboats by European powers off the coast of Venezuela and the occupation of the customs houses of several Caribbean nations (including Puerto Rico) by US Marines, on to the establishment of creditor control over the public finances of Greece, Turkey, Egypt and several other Mediterranean countries.

By and large, however, it was the impersonal power of haute finance — operating through the abstract disciplining mechanism of the bond market and the fiscal straitjacket of the gold standard — that enforced compliance. As Polanyi poetically put it, “the Pax Britannica held its sway sometimes by the ominous poise of a heavy ship’s cannon, but more frequently it prevailed by the timely pull of a thread in the international monetary network.”

3a) The Financialization of the World Economy

World War I brought this Pax Britannica and the associated “dictatorship of finance capital” to a violent end. Despite a fleeting financial resurgence in the roaring 1920s, the Great Depression and the mass destruction wrought by World War II finally led to the total collapse of international capital markets. Strict financial regulations imposed during the 1930s and the international monetary regime established at Bretton Woods at the end of the war briefly brought finance back under public control, leading to a short-lived period of “financial repression” in which interest rates were deliberately held close to or below inflation so as to stimulate industrial production and inflate away enormous war debts. The three decades that followed are often described as the “golden age of capitalism,” as they were marked by exceptionally rapid growth.

But after this postwar expansion had gradually begun to falter under the weight of a set of systemic contradictions in the late 1960s, the Keynesian compromise between capitalist markets and state control over money and finance finally came undone with Nixon’s suspension of the convertibility of the dollar into gold in 1971 and the subsequent Volcker Shock of 1979, which jacked up interest rates to suppress inflation. In the following decade, neoliberal governments in the US and UK set out to repurpose central banks to focus narrowly on “sound money,” to liberalize capital accounts and deregulate financial markets, and to purge the Bretton Woods institutions — the IMF and World Bank — of their Keynesian legacy and restructure them into international debt collection agencies and enforcers of fiscal discipline, “sound” institutions and investor-friendly policies. The international debt crises of the 1980s and 1990s marked a turning point in this respect, with finance reclaiming its stranglehold over the periphery. This time the impersonal force of market discipline and IMF loan conditionality were generally sufficient to enforce debtor compliance; a development that is reflected in the dramatic decline in sovereign defaults.

The resultant financialization of the world economy radically escalated the long-term trend inherent in capitalist development towards what David Harvey has called “space-time compression.” For the sake of comparison: it took Florentine bankers many weeks to deliver a letter of credit by ship from Pisa to Ipswich or Bruges. The Rothschilds significantly sped up the process by relying on carrier pigeons to communicate news and price changes between different branches. The development of commercial telegraphy transformed international trading in the era of haute finance. But it is only with the digital revolution of recent decades that we witness the emergence of a hyper-charged, extra-mobile and highly abstract financial universe that is governed by the speed of fiber optic communication and the impersonal algorithms of complex super-computers as much as it is by the “animal spirits” of individual traders. For the possible consequences of such automated trading, just consider the 36-minute trillion-dollar flash crash of May 6, 2010.

Together with the liberalization of capital flows and the deregulation of financial markets, these technological innovations fully unleashed Schumpeter’s “gale of creative destruction”: over the last thirty-five years, financial crises have become more frequent and more intense than in any other historical period. The same process has also eroded the sovereignty and autonomy of nation states, taking away much of the decision-making authority of government. Territorially delimited and slow-moving, democratic procedures can no longer keep up with the instantaneous and “liquid” logic of high-frequency trading. While citizens get to vote on their government once every so many years, investors now get to vote on government policy every nanosecond. The result is to place democratic forms of government at a distinct disadvantage to unaccountable technocratic forms of governance. As the response to the latest crisis has confirmed, the transnational institutions erected in recent decades — most importantly the European Union — have been geared towards the efficient administration of this highly globalized and financialized world order, not towards its democratization.

3b) The Financialization of Everyday Life

But with the resurrection of global finance in this latest phase of capitalist development we also witness a further expansion in the sphere of financial influence. On top of the deeply rooted state-finance nexus and the increasing dependence of companies and developing countries on all kinds of financial operations, finance now extends its reach into the very fabric of modern society and every aspect of social life. This financialization of everyday life endows financial elites with an even more central role in the operating logic of capitalist society — rendering not just states and firms but all individuals, households and communities increasingly dependent on financial operations for their social reproduction: from student finance to bank deposits, insurance policies to credit cards, mortgage loans to retail investment, payday advances to pension schemes.

In the process, financial rationalities, subjectivities and imaginaries increasingly begin to protrude into how people work, live, speak, dream and interact with one another. In our highly globalized, financialized and digitized 24/7 information economy, everything has to be quantifiable and measurable to justify its existence. As the abstract expression of value, money itself thus becomes an ever-more important mechanism of social control. Deleuze perceptively observed this transformation in his famous Postscript in the early 1990s, when he wrote that “man is no longer man confined, but man in debt.” As finance steadily expands its reach, no stone is left unturned. Under neoliberalism, the logic of the moneylenders gradually takes over as the governing logic of our very existence. The resultant anxieties over due dates, interest rates, overdrafts, house prices, enforcement agents, home repossessions and credit scores are destroying lives and communities around the globe: from the millions of evicted families in Spain and the US to the mass suicides of indebted farmers in India.

Financialization therefore completes the rule of finance by firmly establishing a “global bankocracy” at the apex of the capitalist world-system and extending its (de)regulating presence from politics and the economy to every nook and cranny of modern society. If the first phase of capitalism was marked by the “alienation of the state” and the second by the penetration of finance into industry and empire, the third phase is marked by the wholesale subsumption of the global political economy and of every aspect of our lives under the rationality of the financial markets. More than ever before, the system’s modus operandi is abstract, impersonal, untouchable. Today, finance hardly ever needs to reveal its true face to exert its authority; Greece was actually the exception. Most of the time the global bankocracy is content to quietly operate in the background, shaping the conditions of possibility under which everyone else — states, firms and households — is forced to secure their continued existence.

Defeating the Global Bankocracy

All of this goes to show that financial impunity is not merely due to some failure of the regulatory regime, nor should it be reduced to the moral failings of individual bankers. While regulators may have been “asleep at the switch” in the years preceding the crisis, and while certain traders and executives have certainly displayed criminally irresponsible or morally repulsive behavior both before and after, the overwhelming power of finance is about much more than regulatory capture or personal greed. The real sources for society’s subservience to the interests, ideas and imaginaries of private bankers lie much deeper — in the essence of what capitalism is all about as a historical social order: the accumulation of capital through the maximization of private profit.

In this sense, the rule of finance is no mere accident of history; it is a deeply entrenched and recurring feature of capitalist development that seems impossible to fully extirpate from the nature of the beast. The struggle against the corrupting influence of big banks on the democratic process is therefore necessarily a struggle against the very substance of the profit-driven financial system and of contemporary capitalism more generally. It follows that the “politics of resentment” and its logic of moral outrage will do little to improve the situation. Similarly, tinkering at the margins through piecemeal reforms and regulations is unlikely to dramatically alter the course of history.

Instead, what is needed is deep, structural change that abolishes the exorbitant privilege of private money creation and removes the profit-motive from the allocation of credit and investment altogether, placing the public function of credit-provision under direct democratic control. To make the economy work for “real people,” as well as their wider communities and the natural environment, the opposition will need to do much more than clamor for retribution or express its resentment at the bankers: it will need to start by rebuilding its collective power from below so that it can begin to form a democratic counterweight to the rule of finance, while simultaneously opening up prefigurative spaces for the creation of and experimentation with alternative monetary and financial forms.

While these observations may seem self-evident to those engaged in the various movements against the class power of the 1 percent, it turns out that some of the world’s leading critics of finance — including the otherwise astute Wolfgang Streeck — have pinned their only remaining hopes exactly on such fleeting outbursts of moral indignation, hoping that angry protests will somehow push policymakers to pursue progressive reforms that will put finance back on a leash and return the world to a more palatable form of capitalism. “Express your disgust,” Streeck recently advised the readers of ROAR Magazine when asked what can be done to resist the rule of finance, “and don’t be afraid of appearing emotional, since emotional protest is what technocrats are most afraid of.”

But the time for emotional self-expression has long since passed. If the defeat of the Greek OXI is anything to go by, the broader left will need to go far beyond the populist veneer of moral outrage and emotional protest. To truly turn the tables on the 1 percent, we will need to start thinking very hard about what it would mean to actually build strong, inclusive and enduring social movements; to construct a common political project capable of striking at the heart of the bankers’ regime; to dismantle the institutional foundations of global finance from below; to strengthen the autonomy of democratic procedure, economic production and social reproduction from the financialized logic of the world economy; to radically overhaul the present monetary system and rethink the capitalist money-form altogether; and ultimately to replace the concentrated, centralized and profit-driven finance industry with a thoroughly democratized, decentralized and non-profit credit system centered on collectively-owned and self-managed institutions like public investment funds, mutual savings banks and community-based credit unions. Since such cooperative non-profit lenders should focus their efforts on bankrolling the transition towards an inclusive, egalitarian, ecological and communal economy, the struggle for the democratization of finance cannot be uncoupled from broader emancipatory struggles for popular control over production, exchange and the commons.

There is unfortunately no space here to discuss the inevitable challenges and infinite complexities involved in the ambitious pursuit of such a post-capitalist future — a vast and contested subject that easily merits an entire ROAR issue of its own. But about this there can now be little doubt: as long as we continue to tinker on the margins and refuse to look towards radically different horizons, the next 800 years of moral outrage are unlikely to take us anywhere new.

Source URL — https://roarmag.org/magazine/defeating-the-global-bankocracy/

Next Magazine article

The Potential of Debtors’ Unions

- Debt Collective

- September 21, 2016

The “Golden Noose” of Global Finance

- Fanny Malinen

- September 21, 2016

Digital subscriber

Digital subscriber  Print & Digital subscriber

Print & Digital subscriber